Confidential. © 2014 Mandalay Digital Group, Inc. Page 1 End to End Mobile Content Solution for Carriers and OEMs Investor Presentation May 2014 NASDAQ: MNDL www.mandalaydigital.com

Confidential. © 2014 Mandalay Digital Group, Inc. Page 2 Safe Harbor Statements. Statements in this presentation concerning future results from operations, financial position, economic conditions, product r ele ases and any other statement that may be construed as a prediction of future performance or events, including without limitation statements regarding future profitability and expect ed fiscal 2014 and 2015 revenues, carrier (including Tier 1 carrier) relationships and product deployment and ramp up are “forward - looking statements” (within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended), which involve known and unknown risks, uncertainties and other facto rs which may cause actual results to differ materially from those expressed or implied by such statements. We claim the protection of the safe harbor contained in the Private Secur iti es Litigation Reform Act of 1995 related to these forward looking statements. These factors include the inherent challenges in converting discussions with carriers into contractual relationships and deploying our key products within large enterprises such as major carriers in a timely manner, product acceptance of new products in a competitive marketplace, the p ote ntial for unforeseen or underestimated cash requirements or liabilities, the impact of currency exchange rate fluctuations on our reported GAAP financial statements, the Co mpany’s ability as a smaller company to manage international operations, its ability given the Company’s limited resources to identify and consummate acquisitions, varying and often unpredictable levels of orders, the challenges inherent in technology development necessary to maintain the Company’s competitive advantage such as adherence to release sch edu les and the costs and time required for finalization and gaining market acceptance of new products, changes in economic conditions and market demand, rapid and complex changes oc cur ring in the mobile marketplace, pricing and other activities by competitors, and other risks including those described from time to time in Mandalay Digital Group's filings on Fo rms 10 - K and 10 - Q with the Securities and Exchange Commission (SEC), press releases and other communications. Use of Non - GAAP Financial Measures. Adjusted EBITDA is calculated as income (loss) from continuing operations before interest expense, foreign exchange gains (lo sse s), financing and related expenses, debt discount and debt settlement expense, gain or loss on extinguishment of debt, acquisition and integration costs, income taxes, asset impai rme nt charges, depreciation and amortization, stock - based compensation expense, change in fair value of derivatives, and accruals for discretionary bonuses. Since Adjusted EBITDA is a no n - GAAP measure that does not have a standardized meaning, it may not be comparable to similar measures presented by other companies. Readers are cautioned that Adjusted EBITD A s hould not be construed as an alternative to net income (loss) determined in accordance with U.S. GAAP as an indicator of performance, which is the most comparable measure un der GAAP. Adjusted EBITDA is used by management as an internal measure of profitability. We have included Adjusted EBITDA because we believe that this measure is used by cer tai n investors to assess our financial performance before non - cash charges and certain costs that we do not believe are reflective of our underlying business. A reconciliation of Adjuste d EBITDA to U.S. GAAP net income is expected to be included in the press release announcing the results of our second fiscal quarter, however such reconciliation to future net inc ome is not currently available without unreasonable effort. The information that is unavailable is primarily asset impairment and expenses related to stock - based compensation; it is probab le that when such amounts are available they will result in a significant GAAP net loss for our second fiscal quarter notwithstanding our expected Adjusted EBITDA results.

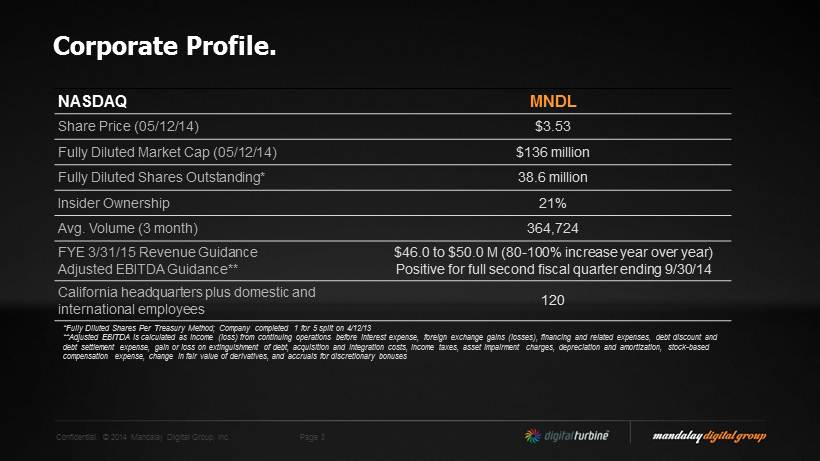

Confidential. © 2014 Mandalay Digital Group, Inc. Page 3 NASDAQ MNDL Share Price (05/12/14) $3.53 Fully Diluted Market Cap (05/12/14) $ 136 million Fully Diluted Shares Outstanding* 38.6 million Insider Ownership 21 % Avg. Volume (3 month) 364,724 FYE 3/31/15 Revenue Guidance Adjusted EBITDA Guidance** $46.0 to $50.0 M (80 - 100% increase year over year) Positive for full second fiscal quarter ending 9/30/14 California h eadquarters plus domestic and international employees 120 Corporate Profile. *Fully Diluted Shares Per Treasury Method; Company completed 1 for 5 split on 4/12/13 **Adjusted EBITDA is calculated as income (loss) from continuing operations before interest expense, foreign exchange gains (losses), fi nan cing and related expenses, debt discount and debt settlement expense, gain or loss on extinguishment of debt, acquisition and integration costs, income taxes, asset impai rme nt charges, depreciation and amortization, stock - based compensation expense, change in fair value of derivatives, and accruals for discretionary bonuses

Confidential. © 2014 Mandalay Digital Group, Inc. Page 4 The Company.

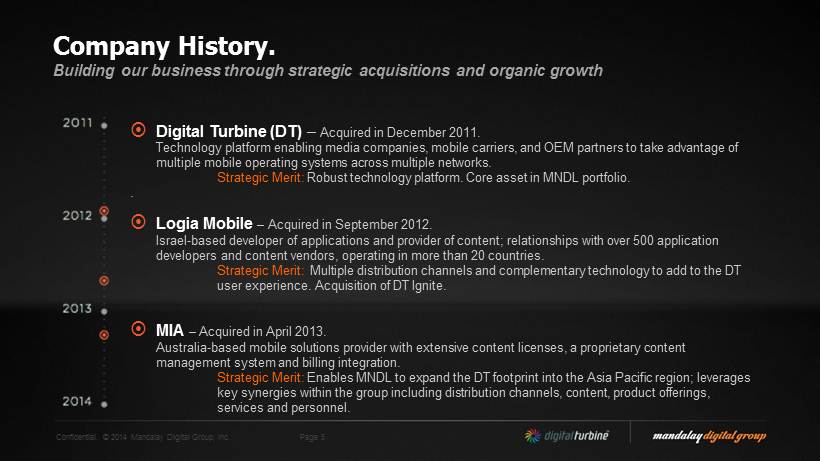

Confidential. © 2014 Mandalay Digital Group, Inc. Page 5 Digital Turbine ( DT ) – Acquired in December 2011. Technology platform enabling media companies, mobile carriers, and OEM partners to take advantage of multiple mobile operating systems across multiple networks . Strategic Merit: Robust technology platform. Core asset in MNDL portfolio . . Logia Mobile – Acquired in September 2012. Israel - based developer of applications and provider of content; relationships with over 500 application developers and content vendors , operating in more than 20 countries . Strategic Merit: Multiple distribution channels and complementary technology to add to the DT user experience. Acquisition of DT Ignite. MIA – Acquired in April 2013. Australia - based mobile solutions provider with extensive content licenses , a proprietary content management system and billing integration. Strategic Merit: Enables MNDL to expand the DT footprint into the Asia Pacific region; leverages key synergies within the group including distribution channels, content , product offerings, services and personnel. Company History. Building our business through strategic acquisitions and organic growth

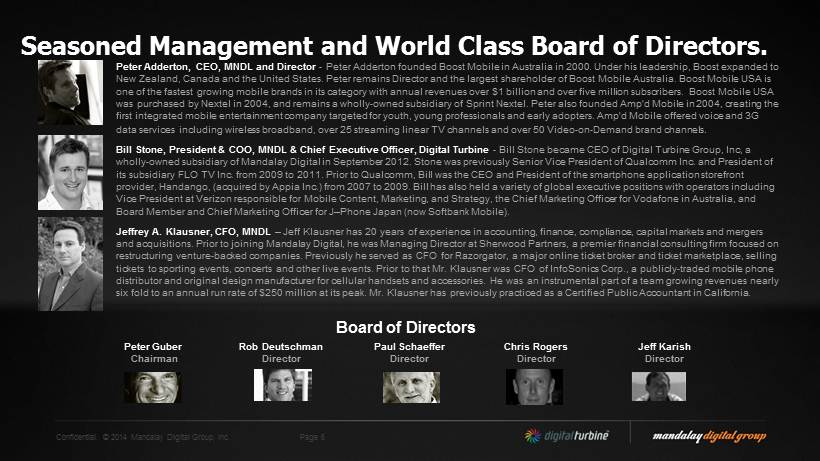

Confidential. © 2014 Mandalay Digital Group, Inc. Page 6 Seasoned Management and World Class Board of Directors. Peter Adderton , CEO, MNDL and Director - Peter Adderton founded Boost Mobile in Australia in 2000. Under his leadership, Boost expanded to New Zealand, Canada and the United States. Peter remains Director and the largest shareholder of Boost Mobile Australia. Boos t M obile USA is one of the fastest growing mobile brands in its category with annual revenues over $1 billion and over five million subscribe rs. Boost Mobile USA was purchased by Nextel in 2004, and remains a wholly - owned subsidiary of Sprint Nextel. Peter also founded Amp'd Mobile in 2004, creating the first integrated mobile entertainment company targeted for youth, young professionals and early adopters. Amp'd Mobile offered voice and 3G data services including wireless broadband, over 25 streaming linear TV channels and over 50 Video - on - Demand brand channels . Bill Stone, President & COO, MNDL & Chief Executive Officer, Digital Turbine - Bill Stone became CEO of Digital Turbine Group, Inc , a wholly - owned subsidiary of Mandalay Digital in September 2012. Stone was previously Senior Vice President of Qualcomm Inc. and P resident of its subsidiary FLO TV Inc. from 2009 to 2011. Prior to Qualcomm, Bill was the CEO and President of the smartphone application st orefront provider, Handango , (acquired by Appia Inc.) from 2007 to 2009. Bill has also held a variety of global executive positions with operators including Vice President at Verizon responsible for Mobile Content, Marketing, and Strategy, the Chief Marketing Officer for Vodafone i n A ustralia, and Board Member and Chief Marketing Officer for J – Phone Japan (now Softbank Mobile). Jeffrey A. Klausner , CFO, MNDL – Jeff Klausner has 20 years of experience in accounting, finance, compliance, capital markets and mergers and acquisitions. Prior to joining Mandalay Digital, he was Managing Director at Sherwood Partners, a premier financial consu lti ng firm focused on restructuring venture - backed companies. Previously he served as CFO for Razorgator , a major online ticket broker and ticket marketplace, selling tickets to sporting events, concerts and other live events. Prior to that Mr. Klausner was CFO of InfoSonics Corp., a publicly - traded mobile phone distributor and original design manufacturer for cellular handsets and accessories. He was an instrumental part of a team gro win g revenues nearly six fold to an annual run rate of $250 million at its peak. Mr. Klausner has previously practiced as a Certified Public Accountant in California. Board of Directors Peter Guber Chairman Rob Deutschman Director Paul Schaeffer Director Chris Rogers Director Jeff Karish Director

Confidential. © 2014 Mandalay Digital Group, Inc. Page 7 The Opportunity.

Confidential. © 2014 Mandalay Digital Group, Inc. Page 8 THE MARKET IMPLICATION Subscribers: • Over 6 Billion Global Subscribers / 4.5B in emerging markets. • ~300M in USA. Enormous Market Opportunity: • While optics do matter, US is only ~5% of market. Devices/Operating Systems: • Google ’ s Android operating system approaching 1B devices. • 1.9B devices sold in 2013; Apple is on only ~195M. • More than 3B to be sold in next 24 months. • Android ~75% of new Smartphone market share. • Crowded space of operating systems trying to compete with Apple and Google (e.g. Mozilla, Tizen , Microsoft, etc ). Android is where device OS growth is happening. While capturing attention and hype, Apple is a relatively small % of global devices. Common standards such as HTML5 best path to work ‘ horizontally ’ across all platforms vs. ‘ betting ’ on winners and losers. Mobile Content, Billing and Apps: • Mobile Content spending ~$60B in 2013 with y - o - y growth of 30%. • Operator Billing to grow 500% from 2012 - 2017 ($2.3B to $13B). • Mobile app revenue expected to reach $46B by 2016. • Mobile advertising to grow from $13B in 2013 to $42B by 2017. Mobile applications driving mobile monetization. Global Revenues: • Operators >$2T. • Samsung ~$250B ($70B mobile). • Apple ~$160B. • Google ~$50B. • Facebook ~$5B. Operators have the most to gain and lose. Mobile Market Opportunity. Sources: IDC, Gartner, Strategy Analytics, Jupiter, Ovum

Confidential. © 2014 Mandalay Digital Group, Inc. Page 9 MNDL Ripe to Capitalize From Recent Market Trends. Macro Trend 1. Google launch of KitKat version of Android, Google Play removed from Vodafone 2. Facebook on $ 1BN run - rate for CPI on mobile 3. Considerable M&A activity, including recent acquisition of WhatsApp by Facebook for $19BN 4. Carriers have tried to vertically integrate to distribute applications directly and build their own UI/UX and have failed – rendering them a ‘dumb pipe’ with little content monetization opportunity 5. Google, Apple and Microsoft provide no subscriber analytics to the carriers. Mandalay Opportunity 1. Carriers, OEMs and application developers must increase their competitive positioning against Google – exactly what DT’s suite of products enables 2. Operators currently NOT participating in this revenue stream – DT Ignite, IQ and Marketplace allow operators to take share in mobile application installs 3. Validation of the DT strategy and focus helping to drive increased customer momentum 4. DT product suite gives carriers the control and differentiation back while not incurring the costs, overhead and distraction 5. DT product suite collects and stores subscriber activity on top of any mobile device or OS (agnostic to platform).

Confidential. © 2014 Mandalay Digital Group, Inc. Page 10 CPI Advertising Driving Meaningful Mobile Growth. ▪ FB stock hits low of $17.73 on September 4, 2012 ▪ Launches app install ads on October 17, 2012 ▪ 350 million app installs through end of Q1 2014 ▪ 609 million mobile daily active users (43% y - o - y increase) ▪ Driving more than $1 billion in annual mobile ad revenue from app install ads; mobile ad revenue growing 80% y - o - y Model nascent – Facebook leading the way Sources: Bloomberg, Yahoo Finance, Fool.com

Confidential. © 2014 Mandalay Digital Group, Inc. Page 11 The Products.

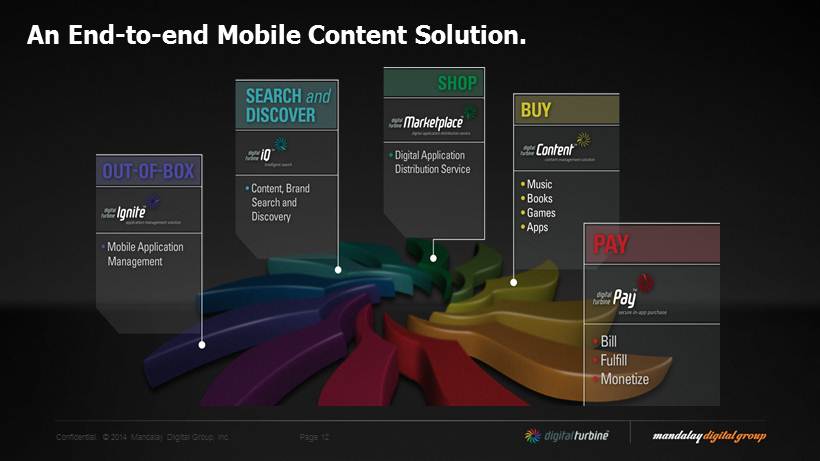

Confidential. © 2014 Mandalay Digital Group, Inc. Page 12 An End - to - end Mobile Content Solution.

Confidential. © 2014 Mandalay Digital Group, Inc. Page 13 Ignite Product Overview. ▪ App management service that enables mobile operators and OEMs to control, manage and monetize the applications that are installed (pre or post) on smartphone devices. ▪ Controls the entire installing process for internal or third party apps. ▪ Allows mobile operators and OEMs to obtain a new advertising revenue stream from pre and post installs. ▪ Offers personalized service packages and application bundles by segment and/or device type. ▪ Provides tools for full analysis and reporting. Control for the carrier and OEM for monetization of their subscriber

Confidential. © 2014 Mandalay Digital Group, Inc. Page 14 Digital IQ Product Overview. ▪ Intelligently unscrambles the myriad of available content to deliver a redefined and personalized user experience (“ UX ”). ▪ Innovative cross - platform user experience and Content Management System (CMS) delivers the app to the user. ▪ Sits atop each of the various operating systems. ▪ IQ App Drawer and IQ search provide capability for multiple CPI app installs across both products. ▪ Intelligent recommendation engine featuring a global marketplace with carrier - branded capability. ▪ Brand pages that support merchandise and ticket purchases. ▪ Single sign - in, one - click purchasing that delivers more on - deck content purchases. Organizing apps through user - specific marketing and search

Confidential. © 2014 Mandalay Digital Group, Inc. Page 15 Content Management Overview. ▪ The only marketplace dedicated for carriers and OEMs to compete with Google Play and iTunes. ▪ Over 100,000 applications serving over 200 million customers in more than 50 countries. ▪ The No. 2 Music Retailer in Australia. ▪ Streaming music product (similar to Spotify ). ▪ Access to 2 million eBook titles, plus reader. ▪ Platform, Ingestion, Content Management, and Reporting provided as Managed Service. ▪ Customers include tier - one operators such as Vodafone, Telstra, SingTel, Telecom Italia, and Cellcom . An alternative and competitive app and content platform

Confidential. © 2014 Mandalay Digital Group, Inc. Page 16 DT Pay Product Overview. ▪ Connectivity to Operators as the “Visa” for processing mobile content transactions. ▪ Enable content providers (e.g. Electronic Arts) to bill directly to customer’s mobile bill. Pre - paid service coming. ▪ Launched in Australia: » Currently $10 million revenue run - rate . » Now launching product in new markets, including Italy (across 4 carriers). Closes the loop on content to billing

Confidential. © 2014 Mandalay Digital Group, Inc. Page 17 The Customers.

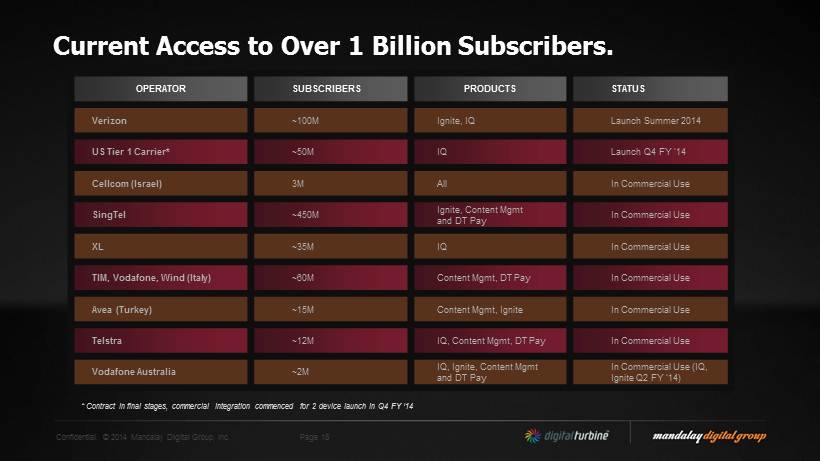

Confidential. © 2014 Mandalay Digital Group, Inc. Page 18 OPERATOR SUBSCRIBERS PRODUCTS STATUS Verizon ~100M Ignite, IQ Launch Summer 2014 US Tier 1 Carrier* ~50M IQ Launch Q4 FY ‘14 Cellcom (Israel) 3M All In Commercial Use SingTel ~450M Ignite, Content Mgmt and DT Pay In Commercial Use XL ~35M IQ In Commercial Use TIM , Vodafone, Wind (Italy) ~60M Content Mgmt , DT Pay In Commercial Use Avea (Turkey) ~15M Content Mgmt , Ignite In Commercial Use Telstra ~12M IQ, Content Mgmt , DT Pay In Commercial Use Vodafone Australia ~2M IQ, Ignite, Content Mgmt and DT Pay In Commercial Use (IQ, Ignite Q2 FY ‘14) Current Access to Over 1 Billion Subscribers. * Contract in final stages, commercial integration commenced for 2 device launch in Q4 FY ‘14

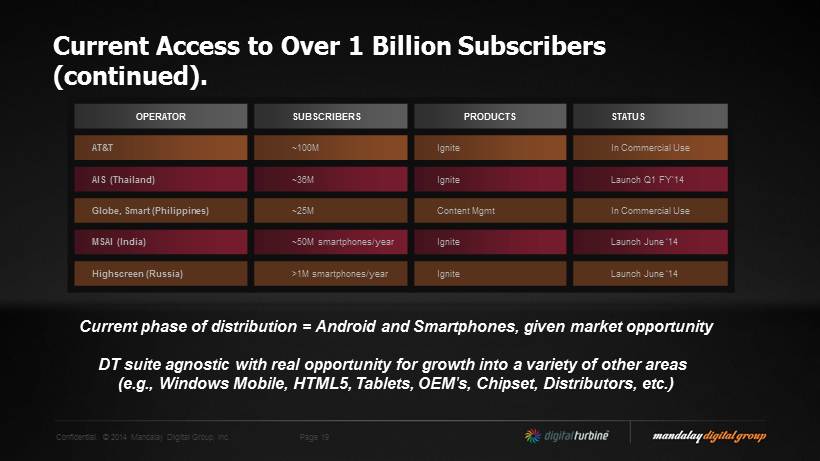

Confidential. © 2014 Mandalay Digital Group, Inc. Page 19 OPERATOR SUBSCRIBERS PRODUCTS STATUS AT&T ~100M Ignite In Commercial Use AIS (Thailand) ~36M Ignite Launch Q1 FY‘14 Globe, Smart (Philippines) ~ 25M Content Mgmt In Commercial Use MSAI (India) ~50M smartphones/year Ignite Launch June ‘14 Highscreen (Russia) >1M smartphones/year Ignite Launch June ‘14 Current Access to Over 1 Billion Subscribers (continued). Current phase of distribution = Android and Smartphones, given market opportunity DT suite agnostic with real opportunity for growth into a variety of other areas ( e.g., Windows Mobile, HTML5, Tablets, OEM's, Chipset, Distributors, etc.)

Confidential. © 2014 Mandalay Digital Group, Inc. Page 20 The Models and Numbers.

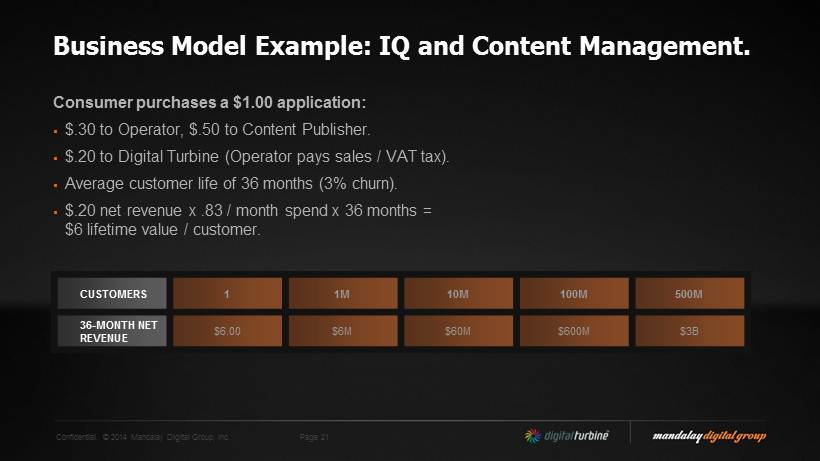

Confidential. © 2014 Mandalay Digital Group, Inc. Page 21 Business Model Example: IQ and Content Management. Consumer purchases a $1.00 application: ▪ $.30 to Operator, $.50 to Content Publisher. ▪ $.20 to Digital Turbine (Operator pays sales / VAT tax). ▪ Average customer life of 36 months (3% churn). ▪ $.20 net revenue x .83 / month spend x 36 months = $6 lifetime value / customer. CUSTOMERS 1 1M 10M 100M 500M 36 - MONTH NET REVENUE $ 6.00 $6M $ 60M $ 600M $ 3B

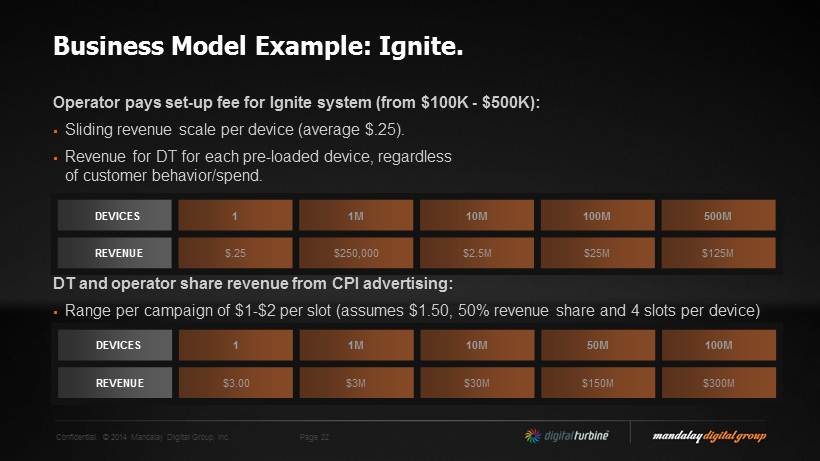

Confidential. © 2014 Mandalay Digital Group, Inc. Page 22 Business Model Example: Ignite. Operator pays set - up fee for Ignite system (from $100K - $500K): ▪ Sliding revenue scale per device (average $.25). ▪ Revenue for DT for each pre - loaded device, regardless of customer behavior/spend. DT and operator share revenue from CPI advertising: ▪ Range per campaign of $1 - $2 per slot (assumes $1.50, 50% revenue share and 4 slots per device) DEVICES 1 1M 10M 100M 500M REVENUE $.25 $250,000 $2.5M $25M $125M DEVICES 1 1M 10M 50M 100M REVENUE $3.00 $3M $30M $150M $300M

Confidential. © 2014 Mandalay Digital Group, Inc. Page 23 The Current Metrics – Recap. • Total global market = ~ 6 billion units (Asia Pacific planning to grow at ~6x greater than the US) • MNDL current total addressable market = ~1 billion units • MNDL technologies currently deployed on 31 million units (~400,000 DT Ignite™ installations completed and additional pending on new phone releases) • MNDL products and technologies used on 2.0 - 2.5 million unique devices, or an average of 2.25 million per month • MNDL realized ~ $3.00 in ARPU with varying margins versus an industry average $ 1.00 • Management focus – INCREASING DEPLOYMENTS and UNIQUE USAGE

Confidential. © 2014 Mandalay Digital Group, Inc. Page 24 Summary Financials. • Completed $20mm (gross proceeds) raise at $4.10/share in early March 2014, zero debt on balance sheet. • Fiscal 2015 revenue guidance at $46mm to $50mm and Adjusted EBITDA positive for the full second fiscal quarter ending 9/30/14. • DT Ignite key growth driver in Fiscal 2015 – expect deployment on 12 million devices. • Logia + MIA are established and growing content businesses with products and relationships that can be leveraged into other DT products. • Diversified revenue streams combined with scalable business model will generate meaningful profitability.

Confidential. © 2014 Mandalay Digital Group, Inc. Page 25 PRODUCT COMPARABLES Out - of - Box (Ignite) Mobile Application Management VMWare acquired Airwatch for $1.2BN in cash. IBM acquired Fiberlink for approximately $130M in cash. Citrix acquired Zenprise for $355M in cash. Search and Discovery (IQ) Everything.me raises $35M at $200M valuation nil revenue. Shop and Buy (Marketplace, Books, Music, etc.) Spotify valued at $3B with ~$250M revenue. Glu Mobile (games) $180M market cap. Billing (DT Pay) Gemalto acquired Ericsson IPX for $60M. Amdocs acquired MX Telecom for $104M. Compelling Valuations. Sources: Yahoo, CNN, Reuters , Doat Media, Google, and Tech Crunch

Confidential. © 2014 Mandalay Digital Group, Inc. Page 26 Contacts. Investor Relations Andrew Schleimer Mandalay Digital Group Direct: 646 - 845 - 7335 Mobile: 646 - 584 - 4021 a.schleimer@mandalaydigital.com Laurie Berman PondelWilkinson Inc. Direct: 310 - 279 - 5962 Mobile: 310 - 867 - 4365 lberman @pondel.com |